Tharisa (LSE:THS) delivered a strong improvement in financial performance for the six months ended 31 March 2026, with revenue increasing 28% to US$359.4 million and EBITDA rising sharply to US$104.3 million. Net profit after tax more than doubled to US$46.6 million, while earnings per share advanced to 15.8 US cents. The group also generated robust operating cash flow of US$96.4 million and invested US$103.5 million in capital expenditure, including ongoing development work at the Karo Platinum project.

The mining group said its operations maintained an exemplary safety record, reporting negligible lost time injury rates across its major assets. Tharisa added that expanded underground development activities at the Tharisa Mine, alongside continued progress at Karo Platinum, reinforce its long-term growth ambitions and multi-generational mining strategy. Supported by the stronger trading backdrop and confidence in the business outlook, the board approved an increased interim dividend of 2.5 US cents per share. The company also confirmed it has until 31 December 2026 to comply with updated JSE governance requirements that disallow an executive chairperson structure.

More about Tharisa

Tharisa is a vertically integrated mining company focused on platinum group metals and chrome concentrates. Its core assets include the Tharisa Mine in South Africa and the Karo Platinum project in Zimbabwe, both of which are geared towards supplying critical minerals used in stainless steel manufacturing, emissions reduction technologies and the global energy transition.

Elon Musk’s SpaceX has officially outlined plans to float on the US stock market, giving public investors the opportunity to buy and trade shares in the aerospace giant.

The company develops rockets, operates the Starlink satellite broadband network, and also controls Musk’s controversial artificial intelligence business xAI.

Trading under the ticker symbol SPCX, the initial public offering (IPO) is expected to become the largest listing ever seen on Wall Street and could launch as early as next month.

The deal could also push Musk — already the world’s richest individual — into trillionaire territory due to the size of his stake in SpaceX.

SpaceX has placed its valuation at around $1.25tn, meaning Musk’s controlling ownership could be worth upwards of $600bn.

Last year, the Tesla chief became the first person in history to surpass a personal fortune of $500bn.

A successful public debut for SpaceX could now lift his overall wealth above the $1tn threshold.

IPO filing exposes SpaceX financial performance

The filing gives investors one of the most detailed snapshots yet of SpaceX’s finances.

In 2025, Space Exploration Technologies — the company’s formal corporate name — generated revenue of $18.6bn (£13.8bn) while recording a net loss of $4.9bn.

During the first quarter of this year, the business reported sales of $4.7bn but posted another net loss, this time totaling $4.3bn.

Company filings show total assets of $102bn, including rockets, launch systems, and equipment, alongside debt liabilities of $60.5bn.

Ruth Foxe-Blader, managing partner at US venture capital firm Citrine Venture Partners, told the BBC “it’s not shocking for a project like this to be loss making, even at the point of IPO”.

She added that the anticipated flotation remained “extremely exciting”.

“SpaceX is just an absolutely sprawling, enormous project with so many different selling points, and so many points that really point to the future.”

Legal disputes and mounting scrutiny

SpaceX disclosed that it expects to incur more than half a billion dollars in legal expenses tied to numerous active claims and lawsuits.

Among the cases are “multiple lawsuits” accusing Grok — the chatbot created by xAI — of being used to generate sexualized deepfakes involving real women and girls.

Musk has previously stated that he intends to fold xAI into SpaceX and continue his artificial intelligence ambitions under the aerospace company.

The group also owns X, the social media platform formerly known as Twitter, which Musk acquired in 2022.

Other legal matters outlined in the IPO filing include patent infringement allegations, accusations related to noncompliance with European Union content moderation rules, music copyright claims, and lawsuits tied to data breaches.

AI expansion and OpenAI rivalry

The filing also disclosed financial details surrounding a newly signed partnership between SpaceX and AI rival Anthropic, the developer behind Claude.

Under the agreement, Anthropic will pay $15bn annually for access to data centres located in the southern United States that support Musk’s xAI operations, which were recently brought under SpaceX ownership.

Despite controversy surrounding Musk’s AI ventures, SpaceX’s launch operations and Starlink business continue to dominate their sectors, maintaining a sizable advantage over rivals.

The IPO filing was released just days after Musk lost a closely watched legal fight against OpenAI and chief executive Sam Altman.

Musk had alleged that Altman breached a non-profit agreement by turning the ChatGPT creator into a commercial business after Musk had contributed millions of dollars in funding.

Jurors unanimously rejected the claims, ruling that Musk waited too long to file his 2024 lawsuit and that the legal deadline had expired.

During the proceedings, Musk acknowledged that xAI remained much smaller than OpenAI, which is also widely expected to pursue a public listing in the near future.

Political backlash and safety concerns

SpaceX is preparing for another launch of its Starship mega rocket later this week, although the company has also faced criticism over worker safety conditions at several sites.

Musk himself has attracted criticism for his right-wing political views and his close ties to US President Donald Trump, whom he accompanied on a visit to China last week.

The testing programme was designed to determine the most effective processing approach for a planned 50tpd carbon-in-leach gold plant, while also evaluating options for future expansion.

Kavango Resources (LSE:KAV) has completed a metallurgical testing programme on ore samples taken from the Hillside Gold Project in Zimbabwe, delivering encouraging results for the proposed processing operation.

The programme focused on identifying optimal processing parameters and plant design specifications for a 50-tonnes-per-day carbon-in-leach (CIL) gold plant currently under development, with additional consideration given to potential future upgrades in capacity.

Testing across different blends of Nightshift and Bill’s Luck ore produced strong metallurgical recovery rates, with laboratory recoveries exceeding 95% and expected operational recoveries estimated at between 90% and 93%.

Results showed that gold from the Nightshift deposit was entirely non-refractory, while ore from Bill’s Luck contained 91% free-milling gold.

Further analysis identified very limited coarse gold content and low concentrations of elements such as native carbon minerals, copper and zinc, which can negatively impact gold recovery as “gold robbers”.

The programme also included gravity recovery testing using centrifugal concentrators, with recoveries ranging from 50% to 90%.

Gold concentrates were found to be suitable for standard intensive leach processing technologies, delivering recoveries of up to 98% after 24 hours.

According to the company, reagent usage and energy consumption remained within standard operating ranges throughout the testwork.

Kavango carried out the programme alongside Solo Resources and Maelgwyn Mineral Services, while SGS South Africa completed mineralogical analysis and assessments under ISO and South African National Accreditation System-accredited standards.

Eight composite ore blends were prepared to reflect the anticipated feed material for both the 50tpd processing plant currently under construction and a proposed future upgrade to 250tpd capacity.

Among the samples tested, composites C and D achieved laboratory recovery rates of 97% and 96%, respectively.

Gravity recoverable gold testing using three-stage and five-stage processes determined that an optimal grind size of 75 microns delivered the best performance.

The company also completed intensive leach reactor testing in preparation for the possible addition of an elution circuit, with results demonstrating strong leaching efficiency.

Kavango Resources interim CEO Peter Wynter Bee said: “The team is extremely encouraged by these excellent metallurgical testwork results. All processing parameters are considered to be within a normal range, with no excess grinding or reagent consumption requirements.

“This gives us the confidence to continue building the resource base at our Hillside projects, with the goal of increasing gold production via future increases in processing capacity.”

More about Kavango Resources

Kavango Resources is a mining exploration and development company focused on projects in Zimbabwe and Botswana. The company is advancing gold exploration and production initiatives at the Hillside Gold Project while also pursuing opportunities in base and precious metals across southern Africa.

As liquidity drives price action, resilient miners continue producing through the noise

At a mining site, a haul truck carries tonnes of ore out of the ground.

It doesn’t know the price of silver.

It doesn’t care about inflation prints, bond yields, or geopolitical headlines.

Its job is simple: move material from point A to point B.

Whether silver is at $30 or $100, the process continues.

The mine is designed around geology and cost, not sentiment.

But above ground, in financial markets, everything reacts instantly.

Prices move. Positions unwind. Narratives shift.

And suddenly, a falling price is interpreted as a failing asset.

But the truck is still moving.

The ore is still there.

The system hasn’t changed.

Only the perception has.

Markets behave the same way.

When pressure hits, prices don’t simply move. They expose what is liquid, what is leveraged, and what can survive forced selling.

Silver right now is that system under pressure.

It didn’t fail. It revealed the stress around it.

The Move Everyone Thinks They Understand

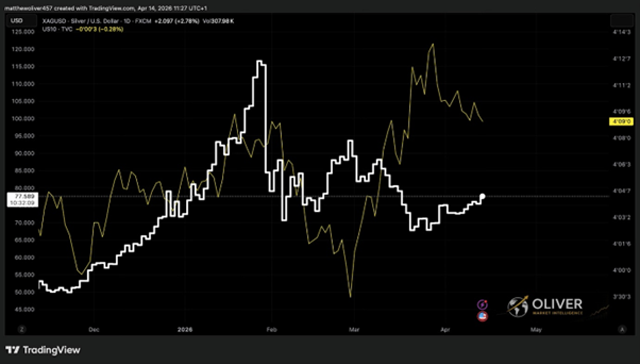

Silver has fallen sharply from its peak. A move like that, especially during geopolitical stress, looks like a breakdown.

The narrative feels straightforward. War risk rises. Oil spikes. Inflation expectations shift. The dollar strengthens. Risk assets sell off.

Silver gets pulled into that move.

On the surface, it looks like demand has weakened or that the rally went too far.

That is the story being told.

But it is not the correct one.

XAGUSD/US10Y – Oliver Market Intelligence

What Is Actually Happening Beneath the Surface

This is not a demand problem. It is a liquidity event.

When stress enters the system, capital does not move calmly. It moves fast and often indiscriminately. Institutions are not asking what they want to sell. They are asking what they can sell.

Silver sits directly in that category.

It is liquid. Widely held. Often part of leveraged positions.

So, when margin requirements rise and volatility spikes, silver becomes a source of cash.

Positions are unwound. Exposure is reduced. Not because the long-term outlook has changed, but because liquidity is required immediately.

This is how modern markets function.

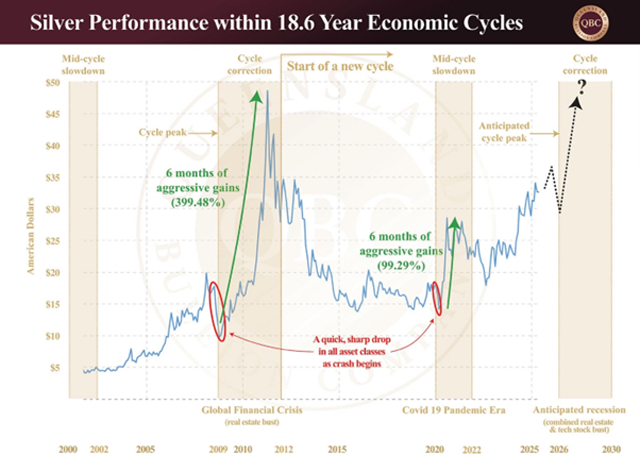

A Pattern That Repeats

This sequence is not new.

In 2008, precious metals sold off alongside equities before recovering.

In March 2020, gold and silver both dropped sharply as markets scrambled for liquidity, then reversed and surged.

What looks like a breakdown is often just the middle phase of a larger cycle.

The difference now is what sits underneath that cycle.

Source: Queensland Bullion Company

The Structural Shift Beneath the Price

While price action in Western markets is being driven by liquidity, the real story is happening elsewhere.

Silver is no longer just a monetary metal.

It is embedded in the industrial system.

The centre of that system is Asia (particularly China) which produces the majority of the world’s solar panels, one of the largest end uses of silver.

This is not cyclical demand. It is structural.

Solar continues to scale. Electric vehicles expand. Electronics remain dependent on silver’s conductive properties.

At the same time, supply is becoming less flexible.

Much of global silver production is a byproduct of mining other metals. That limits how quickly supply can respond to price.

And increasingly, supply is not just geological.

It is political.

Export pathways are tightening. Resource control is becoming strategic.

So, while price has moved lower, the underlying system is doing something very different:

Demand is embedded. Supply is constrained. Control is tightening.

Where the Market Misreads It

This is where the disconnect forms.

Short-term price is driven by liquidity.

Long-term value is driven by structural demand and constrained supply.

Markets tend to misprice that gap.

The focus remains on recent price action, while the more important question is who is buying during that weakness, and why.

The Operators Beneath the Surface

Mining companies sit at the edge of this dynamic.

They are leveraged to price in the short term, but anchored to physical assets in the long term.

When liquidity exits, they can fall alongside everything else.

But their underlying reality does not change nearly as quickly.

Take Silvercorp (AMEX:SVM) (TSX:SVM) as an example.

Across multiple cycles, the company has built a system designed to operate through volatility, not depend on it.

It has produced over 100 million ounces of silver since 2006, generating more than $600 million in profits and over $235 million returned to shareholders. Not just survival, but disciplined capital allocation through the cycle.

Costs matter more than narratives in this business.

More importantly, it operates with all-in sustaining costs below $14 per ounce, allowing it to remain profitable even during weaker price environments .

And that durability is translating right now. In its latest quarter (fiscal Q4 2026 / calendar Q1 2026), Silvercorp delivered record revenue of $147.4 million ( +96% year-on-year) not just riding the move in silver, but amplifying it.

Production isn’t standing still either: 6.8 million ounces over the past year, with organic growth ahead. No reliance on a higher price to justify the story, just steady expansion. Full financial results land May 25.

U.S. stock futures traded higher on Wednesday, signaling a potential rebound for Wall Street after broad declines in the previous session.

Investor sentiment improved as Treasury yields eased from recent highs and crude oil prices moved sharply lower.

Treasury Yields and Oil Prices Decline

The benchmark 10-year Treasury yield retreated after climbing to its highest level in more than a year, while U.S. crude oil futures dropped over 3%.

Oil prices extended losses from Tuesday after President Donald Trump said the conflict involving Iran would end “very quickly.”

“We’re going to end that war very quickly,” Trump said during the annual congressional picnic at the White House on Tuesday. “They want to make a deal so badly.”

“It’s going to happen, and it’s going to happen fast. And you’re going to see oil prices plummet,” the president added.

Even with improving market sentiment, trading volumes could remain muted ahead of Nvidia’s (NASDAQ:NVDA) quarterly earnings report due after the market close.

Nvidia Results and Fed Minutes Awaited

As a key player in the artificial intelligence industry, Nvidia’s earnings and outlook are expected to influence broader market direction.

Market participants are also watching for the release of minutes from the Federal Reserve’s latest policy meeting later in the day.

The minutes from the Fed’s April meeting, where policymakers voted to keep interest rates unchanged after a notably divided debate, may provide additional insight into the future path of monetary policy.

U.S. Stocks Ended Lower on Tuesday

Major U.S. stock indexes finished Tuesday’s session in negative territory after an afternoon recovery attempt faded before the close.

The Nasdaq declined 220.02 points, or 0.8%, to 25,870.71. The S&P 500 lost 49.44 points, or 0.7%, ending at 7,353.61, while the Dow Jones Industrial Average fell 322.24 points, or 0.7%, to 49,363.88.

The selloff coincided with a continued surge in Treasury yields, with the 10-year note reaching its highest level since January 2025.

Inflation and Oil Concerns Continue to Weigh

Persistently elevated oil prices and inflation concerns have continued to pressure bond markets.

Although crude futures pulled back on Wednesday, prices remained above the $100-per-barrel mark amid ongoing geopolitical tensions in the Middle East.

While Trump said he halted a planned strike on Iran following requests from Gulf leaders, investors remain cautious about the possibility of renewed escalation.

The sustained rise in oil prices has increased speculation that the Federal Reserve may be forced to raise interest rates later this year to contain inflationary pressures.

According to CME Group’s FedWatch Tool, markets are currently pricing in a 41.9% chance that rates will end the year a quarter-point higher following the Fed’s final policy meeting.

“While the Nasdaq remains near highs and the broader AI trade is still intact, recent sessions have seen some profit-taking in semiconductors and mega-cap tech as yields rise and positioning looks increasingly stretched,” said Daniela Hathorn, Senior Market Analyst at Capital.com.

She added, “The market is not abandoning the earnings and AI story but the combination of higher oil, higher yields and extremely strong positioning is making it harder for the sector to continue its near-vertical ascent without pauses or pullbacks.”

Pending Home Sales Exceed Forecasts

Economic data released Tuesday showed pending home sales in the U.S. rose more than expected in April.

The National Association of Realtors said its pending home sales index increased 1.4% to 74.8 in April after rising by an upwardly revised 1.7% in March.

Economists had forecast a 0.9% increase following the previously reported 1.5% gain in the prior month.

Gold and Airline Stocks Under Pressure

Gold mining shares fell sharply as gold prices weakened significantly. The NYSE Arca Gold Bugs Index dropped 3.7%, marking its lowest close in more than a month.

Airline stocks also posted steep losses, with the NYSE Arca Airline Index sliding 3.4%.

Housing, brokerage, and computer hardware shares also moved lower, while pharmaceutical, healthcare, and natural gas stocks outperformed the broader market.

European equities traded modestly higher on Wednesday as investors monitored developments in the Middle East, awaited upcoming earnings from Nvidia, and assessed fresh inflation readings from across the region.

Bond markets remained under pressure as traders continued pricing in the possibility of additional interest rate increases from both the European Central Bank and the Federal Reserve before year-end.

Oil prices moved lower after U.S. President Donald Trump stated that the conflict with Iran would end “very quickly.”

Trade and Economic Developments in Focus

On the trade front, the European Union reached a provisional arrangement to eliminate import tariffs on U.S. products, helping the bloc stay on course to meet Trump’s July 4 deadline and avoid steeper duties on European exports.

Economic data released Wednesday showed German producer prices rose 1.7% year over year in April, according to Destatis. The figure reversed a 0.2% decline recorded in March and marked the strongest increase since May 2023, as well as the first annual gain since February 2025.

In the U.K., consumer price inflation eased to 2.8% in April from 3.3% the previous month. The Office for National Statistics attributed the slowdown largely to lower energy bills and softer package holiday prices.

Major European Indexes Advance

The U.K.’s FTSE 100 Index gained 0.2%, while Germany’s DAX Index climbed 0.6%. France’s CAC 40 Index outperformed with a 0.7% increase.

Corporate Movers Across Europe

Stellantis (BIT:STLAM) traded higher after the automaker announced plans to establish a Europe-based joint venture with Dongfeng Motor Group Co., Ltd focused on new energy vehicle production.

Shares of Severn Trent (LSE:SVT) surged after the utility company raised its adjusted earnings outlook for 2026 following strong second-half financial performance.

Retailer Marks & Spencer (LSE:MKS) also posted strong gains after reporting improved second-half profitability.

On the downside, Norway’s Webstep (LSE:0TCZ) dropped sharply after announcing weaker first-quarter profit results due to lower revenue.

Experian (LSE:EXPN) declined in London despite delivering record annual results and unveiling a new $1 billion share repurchase program.

Coats Group (LSE:COA) also moved lower after the industrial thread manufacturer reported a slight decline in revenue on a constant currency basis.

Oil prices moved lower on Wednesday as traders reacted to signs of progress in diplomatic talks between Washington and Tehran, while improving tanker movements through the Strait of Hormuz also eased supply concerns.

By 04:44 ET (08:44 GMT), Brent crude futures for July delivery had fallen 2.5% to $109.25 per barrel, while U.S. West Texas Intermediate crude futures declined 1.9% to $102.35 per barrel. Both benchmarks had already posted losses of roughly 1% in the previous session.

Hormuz tanker activity boosts confidence on supply flows

According to Reuters, citing LSEG and Kpler shipping data, two Chinese-flagged oil supertankers successfully exited the Strait of Hormuz on Wednesday, encouraging hopes that energy shipments through the key maritime route could begin returning to more normal levels.

The South Korean-flagged tanker Universal Winner was also departing the narrow channel near Iran’s southern coastline, which has effectively remained closed to tanker traffic since the outbreak of the U.S.-Israeli conflict with Iran in late February.

U.S. President Donald Trump told lawmakers on Tuesday evening that the Iran war could end “very quickly.” Trump had earlier indicated that he delayed a planned strike against Iran because negotiations with Tehran appeared to be advancing.

Vice President JD Vance also expressed optimism, saying Iran seemed interested in reaching an agreement.

Iran’s latest peace proposal reportedly called for a halt to military operations across all fronts, the withdrawal of U.S. troops from the region and compensation for wartime damages, according to Iranian state media. Washington has so far rejected earlier proposals, maintaining that ending Iran’s nuclear programme remains a critical requirement for any deal.

Traders focus on upcoming U.S. inventory figures

Attention is now shifting toward official U.S. oil inventory data for additional insight into supply conditions amid ongoing global disruptions.

Figures released by the American Petroleum Institute showed a larger-than-expected draw of 9.1 million barrels last week, compared with market expectations for a decline of 3.4 million barrels. API figures are often viewed as a leading indicator for the official U.S. government inventory report due later on Wednesday.

U.S. stockpiles are believed to have declined significantly in recent weeks as exports increased to help offset supply disruptions in overseas markets. Trump has also authorised the release of 172 million barrels from the Strategic Petroleum Reserve to reduce the impact of supply shocks linked to the Iran conflict.

Gold prices remained broadly stable on Wednesday as investors balanced concerns over rising bond yields and a stronger dollar against optimism that diplomatic progress could eventually ease the conflict between the United States and Iran.

At 05:15 ET (09:15 GMT), spot gold traded little changed at $4,480.57 an ounce, while gold futures fell 1.6% to $4,482.80 an ounce.

Higher Treasury yields weigh on gold sentiment

Analysts at Phillip Capital warned that an increase in oil prices linked to the Iran conflict could spark renewed global inflationary pressure and potentially push central banks toward further interest-rate hikes.

Government bond yields have risen sharply in recent days as investors reassessed inflation risks. The yield on the 30-year U.S. Treasury bond — widely regarded as a benchmark for long-term economic expectations — climbed to levels last seen during the global financial crisis nearly twenty years ago. Bond prices generally move inversely to yields.

Rising interest rates tend to reduce demand for non-yielding assets such as gold. Meanwhile, the U.S. dollar remained close to a six-week high, increasing the cost of bullion for foreign buyers.

Investors are also looking ahead to the release of minutes from the Federal Reserve’s April meeting later on Wednesday for additional guidance on the future path of U.S. monetary policy.

Diplomatic hopes continue to support markets

Despite ongoing geopolitical tensions, markets remain hopeful that Washington and Tehran may eventually negotiate an end to the conflict that has persisted for more than two months.

U.S. President Donald Trump told lawmakers on Tuesday evening that the Iran war could end “very quickly.” Trump also said earlier this week that he had delayed additional military strikes against Iran following requests from three Gulf nations.

Vice President JD Vance also struck a positive tone, saying Iran appeared interested in reaching an agreement.

Reuters separately reported that two Chinese oil supertankers exited the Strait of Hormuz on Wednesday, citing vessel-tracking data from LSEG and Kpler. The South Korean tanker Universal Winner was also leaving the strategically important passage near Iran’s southern coast, which has been largely closed to tanker traffic since the conflict between the United States, Israel and Iran escalated in late February.

Oil prices declined as traders grew increasingly optimistic that energy shipments through the Strait of Hormuz may gradually recover. Even so, Brent crude prices remain significantly higher than levels recorded before the conflict began.

“The prospects for U.S.-Iran negotiations remained uncertain, with Iran insisting on its core demands and Trump signaling a possible renewed strike on Iran,” said Neil Welsh, Head of Metals at Britannia Global Markets, in a note.

U.S. equity futures traded little changed on Wednesday as investors balanced mounting inflation concerns tied to the Iran conflict with anticipation surrounding quarterly results from NVIDIA Corporation (NASDAQ:NVDA), which are expected to offer fresh signals on the health of the artificial intelligence sector.

At 03:32 ET, Dow Jones futures were up 27 points, or 0.1%, while S&P 500 futures climbed 0.2% and Nasdaq 100 futures advanced 0.4%. Wall Street’s major indices had closed lower on Tuesday as a sharp rise in government bond yields fuelled concerns that the Iran war could reignite inflation globally and pressure central banks into further rate increases. The 30-year U.S. Treasury yield climbed to its highest level since the global financial crisis nearly twenty years ago.

Trump says Iran conflict may end “very quickly”

Despite ongoing geopolitical tensions, investors continue to hope that diplomatic negotiations between Washington and Tehran could eventually bring the conflict to an end after more than two months of fighting.

U.S. President Donald Trump told lawmakers on Tuesday that the Iran war could end “very quickly.” Earlier this week, Trump said he had delayed additional planned strikes against Iran following requests from three Gulf nations.

Vice President JD Vance also expressed optimism, saying Tehran appeared willing to pursue a deal.

Meanwhile, shipping data cited by Reuters showed that two Chinese-flagged oil supertankers, along with the South Korean tanker Universal Winner, exited the Strait of Hormuz on Wednesday, raising hopes that traffic through the strategically important waterway may gradually resume more normally. Oil prices moved lower on expectations that supply disruptions could ease, although Brent crude remains significantly above levels seen before the outbreak of the conflict.

Nvidia earnings expected to test AI market optimism

Away from geopolitical developments, market attention remains firmly fixed on Nvidia’s quarterly earnings release scheduled after the close of Wall Street trading.

Nvidia has become one of the most closely watched companies in global markets due to its central role in powering artificial intelligence infrastructure. Major technology firms continue committing billions of dollars toward AI-related data centre expansion, leaving expectations for Nvidia’s performance exceptionally high.

Analysts at Vital Knowledge said:

“[S]entiment is bullish around Nvidia given continued strength in overall data center capex spending, the dominance of its core data center GPU franchise, the company’s growing networking footprint, and recent product launches (Groq and Vera) aimed at fending off competition,”.

Still, some concerns remain around increasing competition from chips developed by Google LLC and Amazon.com, Inc., as well as questions over how sustainable the current pace of AI spending will prove to be amid rising memory chip costs.

Markets monitor possible SpaceX IPO filing

Investor attention is also turning toward a potentially historic stock market listing for SpaceX, the aerospace group founded by Elon Musk.

According to reports, SpaceX is considering a June 12 market debut in what could become the largest IPO ever completed. Analysts at Vital Knowledge suggested the company’s prospectus could be released as soon as Wednesday, potentially giving investors deeper insight into SpaceX’s operations and ownership structure.

Federal Reserve minutes due later today

Later in the session, investors will also analyse minutes from the Federal Reserve’s April meeting, which may provide further clues about the policy challenges facing incoming Fed Chair nominee Kevin Warsh.

At that meeting, Federal Reserve officials left interest rates unchanged but expressed concern over the inflationary consequences of the Iran conflict. Policymakers were also divided over whether to continue signalling possible future rate cuts.

Current Fed Chair Jerome Powell stated last month that he intends to remain on the Federal Reserve Board through early 2028, citing “my concern […] about the series of legal attacks on the Fed, which threaten our ability to conduct monetary policy without considering political factors.”

FTSE 100 edges lower as M&S profits fall after cyber disruption while British Land gains on AI-driven office demand.

Market Overview

European markets traded mixed on Tuesday morning, with the FTSE 100 edging lower while Germany’s DAX outperformed following softer UK inflation data and continued expectations for central bank easing later this year. The FTSE 100 slipped 0.06 per cent, while the CAC40 was marginally weaker. In contrast, the DAX gained ground alongside positive momentum from Wall Street, where the Nasdaq and S&P 500 both advanced. Investors continued to assess weakening UK labour market conditions and rising unemployment alongside easing inflation pressures.

Commodity markets reflected a more cautious tone as Brent crude prices eased despite reports of petrol prices reaching fresh highs in the UK. Gold traded slightly lower while copper gained modestly, supported by ongoing expectations of industrial demand linked to infrastructure and AI investment themes. Sterling was mixed against major currencies, slipping against the US dollar and Japanese yen while strengthening modestly against the euro and Swiss franc. Bitcoin also moved higher against sterling.

Market Numbers

FTSE 100: Down (-0.06%), 10,284.78 CAC40: Down (-0.07%), 7,981.760 DAX: Up (0.38%), 24,400.65 NASDAQ: Up (0.40%), 28,931.6 S&P 500: Up (0.19%), 7,366.4

In the Headlines

Cyber Attack Impact – Marks & Spencer (LSE:MKS)

Marks & Spencer reported a sharp decline in annual profits after disruption linked to a cyber attack affected operations and increased costs. The retailer said it was making operational progress despite the setback, with investors closely watching recovery efforts and consumer demand trends.

Office Demand Boost – British Land (LSE:BLND)

British Land posted stronger profits as demand for premium office space improved, driven partly by continued investment linked to artificial intelligence and technology firms. The update reinforced confidence in high-quality commercial property assets despite broader economic uncertainty.

Currencies (vs GBP)

USD: Down (-0.06%), $1.3389 CHF: Up (0.16%), Fr.1.05846 EUR: Up (0.04%), €1.1545 JPY: Down (-0.07%), ¥212.943 AUD: Down (-0.01%), $1.883830 Bitcoin (BTC/GBP): Up (0.73%), £57,738.2

Commodities

Copper: Up (0.17%), 6.2562 Gold: Down (-0.02%), 4,500.22 Brent Crude: Down (-0.90%), 106.765 Natural Gas: Down (-0.61%), 3.2565