What is DealRoom — and why should investors be paying attention?

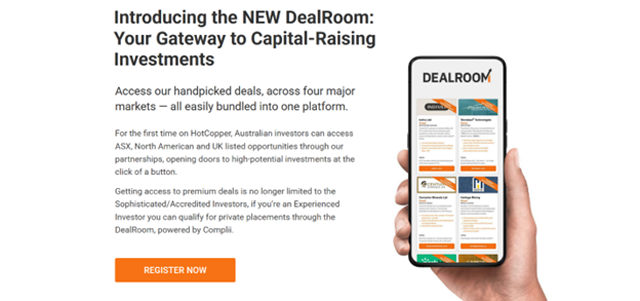

DealRoom is ADVFN’s new dedicated capital-raising platform designed to connect investors directly with pre-IPO opportunities and high-demand private placements across global markets. It gives investors early visibility into capital raises that are often difficult to access, allowing them to evaluate opportunities before they reach the broader market.

What sets DealRoom apart is its scale and reach. Through ADVFN’s global network, investors gain access to opportunities spanning the UK, Australia, and North America, all within a single platform. For investors looking to diversify geographically, access earlier-stage deals, or stay closer to the source of capital formation, DealRoom offers a streamlined and transparent entry point — with no obligation, just opportunity.

With the official launch of DealRoom in the UK, a new and highly engaged investor base can now participate in this growing cross-border investment ecosystem.

A new chapter in global deal flow

The UK expansion marks a significant milestone in DealRoom’s evolution, extending its reach to another major financial market and strengthening cross-border capital connectivity. DealRoom now provides a direct channel between public companies seeking capital and investors searching for early-stage and private market opportunities — regardless of geographic location.

This expansion follows the acquisition of The Market Link by ADVFN, bringing together leading retail investor platforms under one global umbrella, including HotCopper, Stockhouse, ADVFN.com, and InvestorsHub in the United States.

By unifying these platforms, DealRoom can now reach more than 30 million investors annually, creating one of the largest global investor communities focused on small-cap, growth, and emerging opportunities.

“We can match the right investors with the right transactions,” said Tim Sylvester, Director of Capital Markets at HotCopper. “Opening DealRoom to UK investors gives them access to transactions originating in Australia, Canada, and of course the UK itself.”

Borders matter less than investment preferences

As capital markets become increasingly global, DealRoom reflects a broader shift in how companies raise funds and how investors deploy capital. Companies are acquiring assets internationally, pursuing dual listings, and sourcing investors well beyond their home markets.

DealRoom removes geographic barriers by allowing investors to focus on what matters most: sector exposure, deal structure, and risk profile.

“Investor pools are no longer concentrated in one place,” Mr Sylvester said. “DealRoom helps align capital with opportunity, wherever it originates.”

Why now?

Private placements are regaining momentum across major markets, and investor appetite is rising alongside improving capital-raising conditions. Over the next 12 months, DealRoom expects increased activity as public and private companies look to fund growth, acquisitions, and market expansion.

“We’ve seen participation increase dramatically, even in the last few months,” Mr Sylvester noted. “And we expect that momentum to continue.”

For investors, this creates a timely opportunity to gain early insight into upcoming transactions, assess opportunities efficiently, and stay ahead of market developments — without pressure to participate.

Accessing DealRoom

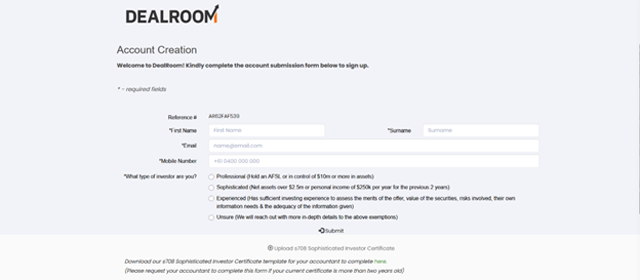

Opportunity is knocking. Investors and companies across the UK, Australia, and North America, can register for DealRoom and begin exploring available opportunities from anywhere in the world.

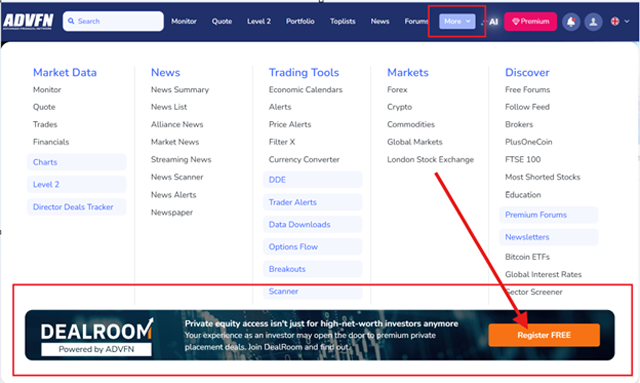

Accessing DealRoom via ADVFN is simple: you can do so by clicking HERE or by selecting it in the ADVFN navigation from the “More” menu.