Predator Oil & Gas Holdings Plc (LSE:PRD) has initiated rigless testing at its MOU-3 well, located in the Guercif region of Morocco. The ten-day program will focus on evaluating the shallow ‘A’ Sand reservoir, with the goal of unlocking additional gas resources. If successful, the operation could accelerate the company’s path to commercialization, taking advantage of Morocco’s attractive gas pricing and investor-friendly fiscal environment. A positive outcome may enhance profitability and reinforce Predator’s strategic position in the Moroccan energy sector.

About Predator Oil & Gas Holdings Plc

Headquartered in Jersey, Predator Oil & Gas Holdings Plc is an exploration and production company with interests in Morocco and Trinidad. In Morocco, the firm is targeting rapid gas monetization through compressed natural gas (CNG) development from its onshore assets. Meanwhile, its operations in Trinidad focus on optimizing output from established onshore oil fields, offering opportunities for both production growth and asset development.

This content is for informational purposes only and does not constitute financial, investment, or other professional advice. It should not be considered a recommendation to buy or sell any securities or financial instruments. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.

U.S. Inflation Rises as Corporate Earnings Fuel Market Highs

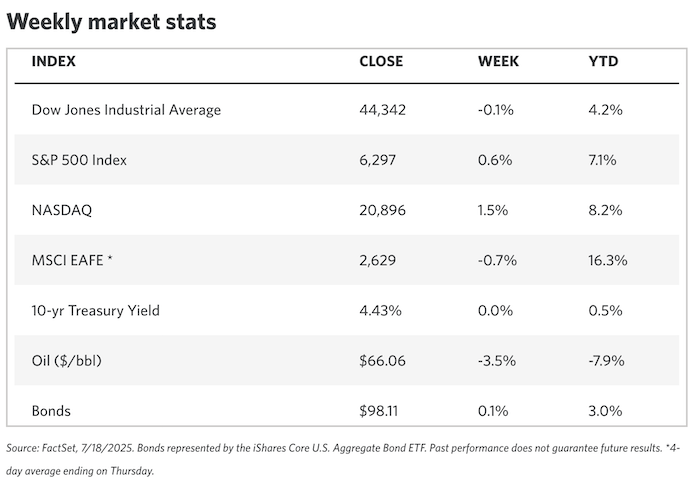

United States

Strong Earnings Lift Markets to New Highs The S&P 500 and Nasdaq Composite both hit new all-time highs last week, driven by strong Q2 earnings and generally positive economic data. The Russell 2000 also rose, while the Dow Jones Industrial Average and S&P Midcap 400 ended slightly lower.

The earnings season kicked off with major banks like JPMorgan Chase and Citigroup reporting better-than-expected results. Later in the week, consumer-facing companies such as PepsiCo, United Airlines, and Netflix also topped forecasts.

NVIDIA rallied after receiving approval from the Trump administration to sell its H2O AI chips to China. The company, which recently hit a $4 trillion market cap, surged on the news.

Inflation Picks Up; Retail Sales Rebound June CPI rose 0.3% month over month—its biggest jump in five months—matching expectations. On a year-over-year basis, inflation accelerated to 2.7%, while core CPI rose to 2.9%, up from 2.8% in May. Prices for household goods, recreation, and footwear saw notable increases, partly offset by declining vehicle prices.

Retail sales rose 0.6% in June, rebounding from May’s 0.9% drop. Midweek market jitters over reports that President Trump might remove Fed Chair Jerome Powell were quickly reversed after Trump denied the rumor.

Corporate Bonds Outperform Treasuries Intermediate- and long-term Treasury yields held steady, while short-term yields edged lower amid speculation around the Fed. Investment-grade corporate bonds outperformed Treasuries, with new issues largely oversubscribed.

Europe

Markets Mixed as Investors Eye Trade Talks The STOXX Europe 600 finished flat, as investors monitored progress in U.S.-EU trade discussions. Italy’s FTSE MIB rose 0.58%, France’s CAC 40 and Germany’s DAX were little changed, and the UK’s FTSE 100 gained 0.57%, helped by a weaker pound.

UK Inflation Surges; Labor Market Softens UK inflation surprised to the upside, rising to 3.6% in June—the highest since January 2024—driven by higher fuel prices. Core services inflation held at 4.7%, showing persistent cost pressures.

The job market weakened. The unemployment rate ticked up to 4.7%, and payrolls fell by 41,000 in June. Wage growth (excluding bonuses) came in at 5.0%, slightly above forecasts but down from 5.3% in May.

Eurozone Industrial Output Rebounds Industrial production in the euro area rose 1.7% in May, beating expectations and reversing April’s 2.2% drop. Strong output in energy, capital goods, and non-durable consumer goods contributed to the gain. Year over year, output rose 3.7%.

The region’s trade surplus widened to €16.2 billion, up from €12.7 billion a year ago, as exports grew and imports fell.

German Sentiment at 3-Year High Germany’s ZEW economic sentiment index rose for the third month in a row, reaching 52.7—the highest since February 2022. Optimism was driven by hopes for EU stimulus and resolution of U.S.-EU trade tensions.

Asia-Pacific

Japan: Modest Gains Ahead of Elections Japanese equities posted moderate gains, with the Nikkei 225 up 0.63% and the TOPIX rising 0.40%. Investors await results from the July 20 Upper House election, which could impact Prime Minister Shigeru Ishiba’s coalition majority.

The 10-year JGB yield rose to 1.53%, while the yen weakened toward 148 per U.S. dollar.

Cooling Inflation, Weak Exports Core CPI rose 3.3% in June, below expectations and down from 3.7% in May, due mainly to lower energy costs. Exports fell 0.5% year over year, missing forecasts, with declines in autos, parts, and pharmaceuticals. A new 25% U.S. tariff on Japanese goods is set to take effect August 1, though bilateral talks are ongoing.

China: Solid GDP, But Risks Loom Mainland Chinese markets advanced, with the CSI 300 up 1.09% and the Shanghai Composite up 0.69%. Hong Kong’s Hang Seng jumped 2.84%.

China’s Q2 GDP grew 5.2% year over year, slightly above expectations, easing near-term pressure for stimulus. However, deflation concerns, soft retail sales, and upcoming U.S. trade deadlines pose headwinds.

The real estate downturn persists: new home prices fell 0.27% in June, while existing home prices dropped 0.61%. Residential sales fell 12.6% year over year—the largest decline in 2025 so far.

Other Key Markets

Indonesia: Rate Cut and U.S. Trade Deal Indonesia’s central bank cut its benchmark rate from 5.50% to 5.25%, citing lower inflation forecasts and the need to support growth. Separately, the U.S. and Indonesia finalized a trade deal that set tariffs at 19%—down from an initially proposed 32%. Indonesia also agreed to purchase Boeing aircraft and import over $20 billion in U.S. energy and agricultural goods.

Peru: Central Bank Holds Steady Peru’s central bank kept its policy rate at 4.50%, as expected. Annual inflation remained at 1.7% in June, with stable 12-month inflation expectations at 2.3%. Policymakers noted that global inflation expectations—particularly in the U.S.—may slow the path back to target inflation locally.

This content is for informational purposes only and does not constitute financial, investment, or other professional advice. It should not be considered a recommendation to buy or sell any securities or financial instruments. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.

U.S. stocks ended Friday on a mixed note, with the S&P 500 closing flat amid renewed trade tensions with Europe. Despite the muted session, the benchmark index posted a gain for the week.

By the closing bell, the Dow Jones Industrial Average fell 142 points (0.3%), the S&P 500 was virtually unchanged, and the NASDAQ Composite ticked up 0.1%.

Market sentiment took a hit after the Financial Times reported that President Donald Trump is considering tariffs of 15% to 20% on goods imported from the European Union. The proposed levy—well above the 10% the EU had hoped for—suggests trade negotiations may have stalled. With the August 1 deadline fast approaching, the move appears designed to pressure the EU into making broader concessions.

Earnings Season Gathers Momentum

Investors continue to digest second-quarter earnings, which have been largely better than expected so far:

American Express (AXP) climbed after the credit card company beat profit estimates, fueled by strong spending from high-income consumers.

3M (MMM) rose after raising its full-year earnings outlook, benefiting from cost-cutting efforts and a shift toward higher-margin products.

Charles Schwab (SCHW) advanced after reporting strong quarterly results driven by asset growth and improved net interest margins.

Netflix (NFLX) delivered solid earnings and raised its revenue guidance for the year, but shares pulled back slightly as results fell short of sky-high analyst expectations. Even so, Netflix stock is up over 43% year-to-date, supported by confidence in its dominance in the streaming sector.

Looking ahead, the earnings calendar remains busy next week, with reports expected from Coca-Cola (KO), Texas Instruments (TXN), Alphabet (GOOGL), and Tesla (TSLA).

Consumer Sentiment Improves as Inflation Expectations Ease

The University of Michigan’s consumer sentiment index rose to 61.8, slightly above expectations of 61.5. One-year inflation expectations dropped to 4.4%, down from 5.0% previously—an encouraging sign for consumers and policymakers.

Recent economic data has shown resilience: retail sales beat forecasts, weekly jobless claims declined, and June inflation remained largely in line with estimates. However, tariffs are beginning to put upward pressure on select consumer goods.

Amid these developments, the Federal Reserve has adopted a cautious, wait-and-see stance. Still, Fed Governor Christopher Waller said Thursday that a rate cut at the Fed’s next meeting could be warranted, citing growing risks to the economy.

Waller also emphasized that the recent inflation uptick driven by tariffs is likely temporary and shouldn’t alter the Fed’s broader policy outlook.

Meanwhile, President Trump continues to push the Fed to act more aggressively in lowering interest rates to support economic growth.

This content is for informational purposes only and does not constitute financial, investment, or other professional advice. It should not be considered a recommendation to buy or sell any securities or financial instruments. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.

European equities exhibited a mixed bag of results on Friday, buoyed in part by encouraging U.S. economic indicators and solid technology sector earnings, which have temporarily eased fears surrounding tariffs.

The German DAX slipped 0.3%, while the French CAC 40 edged up 0.1%, and London’s FTSE 100 gained 0.2%.

On the economic front, German producer prices continued their downward trend, falling for the fourth consecutive month in June, driven by lower energy costs, according to Destatis. The producer price index registered a 1.3% decline year-over-year, accelerating from May’s 1.2% drop.

In corporate news, engineering firm Senior (LSE:SNR) rallied after announcing the sale of its Aerostructures business for up to £200 million and unveiling a £40 million share repurchase plan.

Luxury goods company Burberry Group (LSE:BRBY) also saw its shares climb following a better-than-anticipated performance in first-quarter comparable sales.

Chemical industry heavyweight BASF SE (TG:BAS) rose after finalizing a decade-long natural gas supply contract with Equinor.

Defense contractor Saab (BIT:1SAAB) jumped after reporting stronger-than-expected profits and sales for the second quarter.

Conversely, Salzgitter AG (TG:SZG) shares tumbled after the German steelmaker lowered its full-year outlook due to a sluggish second quarter.

Pharmaceutical giant GSK (LSE:GSK) faced pressure after a U.S. FDA advisory panel advised against approval of its blood cancer treatment, Blenrep.

Lastly, Electrolux, the Swedish appliance manufacturer, dropped sharply despite posting second-quarter operating profits above forecasts.

This content is for informational purposes only and does not constitute financial, investment, or other professional advice. It should not be considered a recommendation to buy or sell any securities or financial instruments. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.

U.S. stock futures indicate a modestly higher open on Friday, potentially extending gains from the past two sessions. Positive economic data and strong corporate earnings are supporting investor optimism despite ongoing trade war concerns.

Shares of 3M (NYSE:MMM) jumped 2.7% pre-market after reporting better-than-expected Q2 results and raising full-year sales guidance. American Express (NYSE:AXP) also looks set for gains following its strong quarterly earnings.

Conversely, Netflix (NASDAQ:NFLX) fell 2.9% pre-market despite beating Q2 estimates, due to a warning about lower operating margins in the second half.

Housing stocks may benefit from a Commerce Department report showing new U.S. residential construction rebounded more than expected in June.

On Thursday, the Nasdaq and S&P 500 reached record closing highs, with the Nasdaq up 0.7%, S&P 500 up 0.5%, and Dow up 0.5%.

Economic reports showed retail sales rose 0.6% in June, beating forecasts, and first-time jobless claims fell to a three-month low of 221,000. Import prices increased less than expected.

Market sectors performing well include networking, oil services, financials, steel, and software. Pharmaceutical and healthcare stocks lagged.

Chris Zaccarelli, CIO of Northlight Asset Management, noted that despite tariff concerns, the strong economy and consumer spending continue to fuel stock market gains.

This content is for informational purposes only and does not constitute financial, investment, or other professional advice. It should not be considered a recommendation to buy or sell any securities or financial instruments. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.

In a bold move to fuse finance with entertainment, CFI Financial Group has been named the Official Online Trading Partner of Etihad Arena, the UAE’s largest indoor venue and a regional hub for world-class events.

The partnership grants CFI premium brand visibility across Etihad Arena’s packed calendar of concerts, sporting spectacles, and cultural showcases. As part of the deal, CFI will operate a dedicated fan activation space, host clients in a luxury hospitalitysuite, and offer VIP experiences including meet-and-greets and exclusive giveaways.

“Etihad Arena has become a regional hub for entertainment, sports and culture, and we are thrilled to join forces with a venue that shares our passion for high performance and innovation,” said Ziad Melhem, CEO of CFI Financial Group.

The collaboration reflects CFI’s strategy to deepen engagement with audiences through lifestyle platforms, complementing its existing partnerships with AC Milan, MI Cape Town, and the Department of Culture and Tourism – Abu Dhabi.

Marcus Osborne, General Manager at Etihad Arena, welcomed the alliance: “This partnership reflects our shared vision of delivering extraordinary experiences to fans while championing innovation and excellence.”

With this latest move, CFI continues to expand its footprint across the MENA region, blending financial literacy with immersive brand experiences and positioning itself as a dynamic force in both trading and entertainment.

Helium One Global Ltd (LSE:HE1) has officially received a mining licence for its Southern Rukwa helium site in Tanzania and secured a £10 million investment from three institutional investors, marking a major step forward in its plans to develop two potentially valuable helium sources.

The AIM-listed exploration company, which also holds a 50% stake in the Galactica-Pegasus venture in Colorado, said the fresh capital will be used to fund upcoming testing activities in Southern Rukwa and support the U.S. project’s progress toward first gas and initial cash flow by Q4.

In addition to the institutional backing, Helium One intends to launch a £1 million retail offering, giving current shareholders a chance to take part in the company’s fundraising efforts.

The £10 million funding, facilitated by Marex Financial, is structured as an advance that can be converted into equity at the investors’ discretion, using a predetermined discount on the company’s share price. Any portion not converted must be repaid within 12 months—either in cash, shares, or a mix of both.

Chairman James Smith described the raise as “an important step” that will help advance both the Tanzania and U.S. projects toward production and revenue generation.

CEO Lorna Blaisse emphasized the significance of the developments, stating that the mining licence approval and new funding represent “a key milestone” for the Southern Rukwa site, particularly at the Itumbula West discovery.

Now holding a 480km² mining licence and operating under the joint venture Songwe Helium, the company is preparing for further testing in the final quarter of the year. This will involve re-entering the previously drilled ITW-1 well and using an electric submersible pump to initiate artificial lift, increasing gas flow and enabling better measurement of helium content in target rock layers.

The results will inform final planning for development and processing infrastructure. Regulatory details for Southern Rukwa are still being finalized, and a formal signing date remains pending. However, the Tanzanian government has already agreed to a 17% free carried interest in the project.

Meanwhile, the Galactica-Pegasus project in Colorado, operated by Blue Star Helium, is also expected to benefit from the new funding, with initial gas production targeted before the year’s end.

This content is for informational purposes only and does not constitute financial, investment, or other professional advice. It should not be considered a recommendation to buy or sell any securities or financial instruments. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.

Global forex broker Exness has abruptly suspended new client registrations in India, sparking concern among traders and affiliate partners. The move, which took effect late last week, blocks access to account creation for users with Indian IP addresses. Visitors are now redirected to a simplified login page, with no option to sign up.

The company has yet to issue a formal statement explaining the decision or clarifying whether the restriction is temporary. Affiliate partners were notified to cease all client acquisition efforts in India, further fueling speculation about the broker’s future in the region.

Despite the registration freeze, existing Indian clients remain unaffected. Users with active accounts can continue trading without disruption, according to current access paths.

India has long been a key growth market for offshore brokers like Exness, which operated locally through affiliates and introducing brokers. However, the country’s tightening regulatory landscape — including stricter oversight from the Securities and Exchange Board of India (SEBI) and the Reserve Bank of India (RBI) — may be prompting a strategic retreat.

As of now, Exness has not indicated whether similar restrictions will be applied in other jurisdictions. The situation remains fluid, with industry observers awaiting further updates.

U.S. stock futures edged up Friday as investors focused on upcoming corporate earnings and economic indicators. Netflix (NASDAQ:NFLX) beat earnings expectations but shares slipped as analysts noted the results fell short of very high hopes. Meanwhile, a key consumer sentiment report is due soon, and Bitcoin advanced after the U.S. House passed three bills aimed at providing clear regulatory guidelines for digital assets.

Futures gain ground

U.S. futures climbed slightly Friday, hinting at a continuation of the previous session’s gains, which were driven by upbeat second-quarter earnings and signs of steady economic growth despite ongoing tariff concerns.

By 03:51 ET, Dow futures were up 64 points (0.1%), S&P 500 futures rose 8 points (0.1%), and Nasdaq 100 futures added 27 points (0.1%).

Wall Street’s main indexes gained Thursday, buoyed by a wave of positive corporate earnings and optimistic executive commentary. Economic data this week also suggests the U.S. economy is picking up speed, though inflation pressures linked to President Donald Trump’s aggressive trade policies persist.

Economists caution that tariffs may raise prices and slow growth, but uncertainty remains about how severe the impact might be.

“[O]ur base case remains that the tariffs ultimately imposed will not cause a recession — though we expect growth to slow,” Capital Economics analysts wrote in a note.

Netflix earnings

Netflix shares dipped slightly in after-hours trading despite solid Q2 earnings and guidance. The streaming giant posted a diluted EPS of $7.19, beating estimates of $7.08, helped by the huge success of its hit series “Squid Game,” according to LSEG data cited by Reuters.

The company also raised its full-year revenue forecast to between $44.8 billion and $45.2 billion, up from $44.5 billion previously.

The improved outlook partly reflects a weaker U.S. dollar, which analysts at Vital Knowledge described as a “low-quality source.”

Investing.com analyst Thomas Monteiro added the guidance “now feels quite conservative,” calling this “problematic for a stock priced for perfection.” Netflix’s shares have surged over 43% this year on expectations it will further solidify its streaming dominance.

Michigan sentiment report on deck

Investors are gearing up for the University of Michigan’s monthly consumer sentiment index, expected to show a slight rise in July with inflation expectations holding steady.

“We’ll see whether 1-year inflation expectations have continued to drop: they are currently at 5%, though opinions diverge sharply between Democrat (very high) and Republican (very low) responders,” ING analysts said in a note.

The report follows strong retail sales and lower-than-expected jobless claims this week, reinforcing signs of a resilient U.S. economy despite tariffs pushing some prices higher.

Fed’s Waller supports rate cut

Amid this backdrop, the Federal Reserve has mostly taken a wait-and-see stance on interest rates. However, Fed Governor Christopher Waller said Thursday that a rate cut at the central bank’s upcoming meeting is justified, citing growing economic risks.

He noted the tariff-driven inflation rise is likely temporary, not a persistent problem.

“It makes sense to cut” the policy rate by 0.25 percentage points at the Fed’s July 29-30 meeting, Waller said at an event.

Waller’s remarks come as Fed Chair Jerome Powell faces increasing pressure from President Trump to quickly reduce borrowing costs. Powell, emphasizing the Fed’s independence, prefers a cautious approach to assess tariffs’ full impact.

Bitcoin rises after U.S. House passes crypto bills

Bitcoin briefly climbed above $120,000 in Asian trading Friday, on track for its fourth straight weekly gain after the U.S. House approved three bills to create a new regulatory framework for cryptocurrencies.

As of 03:52 ET, Bitcoin was up 1.1% at $119,583.3.

The cryptocurrency hit record highs above $123,000 earlier this week but profit-taking and concerns about the bills’ final passage capped gains.

The “GENIUS Act,” passed by a bipartisan 308-122 vote, mandates stablecoin issuers maintain dollar-backed reserves with regular audits, and sets both federal and state oversight.

Two other bills also passed: the CLARITY Act, which aims to clarify whether digital tokens fall under SEC or CFTC jurisdiction; and the Anti-CBDC Surveillance State Act, which prevents the Fed from issuing a central bank digital currency without Congress’s explicit approval.

This content is for informational purposes only and does not constitute financial, investment, or other professional advice. It should not be considered a recommendation to buy or sell any securities or financial instruments. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.

The U.S. dollar edged lower during early trading on Friday but remained poised to secure its second straight weekly gain. A stream of upbeat economic indicators continued to reinforce the belief that the Federal Reserve will hold off on interest rate cuts for now.

As of 04:15 ET (08:15 GMT), the Dollar Index—which tracks the greenback against six major currencies—was down 0.4% at 98.100. Still, it was on pace to finish the week up by approximately 0.7%, extending gains of nearly 1% from the prior week.

Greenback Benefits From Strong Economic Signals

Investor demand for the dollar has stayed firm, fueled by signs of ongoing economic strength in the U.S., which is bolstering the case for the Fed to maintain higher interest rates longer than initially anticipated.

Fresh data on Thursday revealed that retail sales climbed more than forecast in June, while initial jobless claims dropped to their lowest level in three months—both highlighting resilience in the consumer sector.

Earlier this week, figures showed consumer prices increased at their fastest pace in five months, raising the possibility that new tariffs may be contributing to a slight uptick in inflation.

“One of our key calls this summer is that this return to dollar ‘functionality’ reduces the likelihood of new selloffs – unless Trump fires Fed Chair Jay Powell (as Wednesday’s brief dollar collapse showed) or escalates protectionism beyond markets’ current tolerance, particularly against China,” noted analysts at ING in a research note.

“We don’t expect either, and still see some dollar support in the coming months as the 14bp priced into the Fed’s September contract unwinds,” they added.

Market pricing currently reflects around 45 basis points of Fed rate cuts for the remainder of the year—slightly less than the 50 basis points priced in earlier this week.

Friday’s economic docket includes U.S. housing data and the University of Michigan consumer sentiment surveys.

Weak U.K. Growth Data Hits Pound, Euro Recovers

The euro climbed 0.3% to 1.1623 against the dollar, bouncing back after hitting a three-week low of 1.1556 on Thursday. However, it was still facing a 0.6% decline for the week.

German producer price data matched expectations, falling 1.3% year-over-year in June, while eurozone inflation held steady at 2.0%, consistent with the European Central Bank’s target.

Despite subdued inflationary trends in Germany—the bloc’s largest economy—any monetary policy easing by the ECB could be complicated by President Donald Trump’s proposed 30% tariffs on EU imports.

After its June policy meeting, the ECB signaled a likely hold on rates this month. However, ING suggested there’s still potential for surprises.

“That said, the ECB meeting may prove less dull than expected,” said ING. “A cut is highly unlikely given recent communication, but tariff risks and a strong euro could revitalise a dovish front that otherwise seemed settled on a neutral pivot.”

Meanwhile, GBP/USD edged up 0.2% to 1.3432 but was still on track for a 0.5% weekly drop. U.K. economic indicators—including a surprise uptick in the unemployment rate and a monthly contraction in GDP for May—have strengthened expectations for further rate cuts by the Bank of England.

Yen Under Pressure from Political Concerns

The dollar rose 0.1% to 148.63 yen, with the Japanese currency heading toward a 0.8% weekly decline. Markets reacted to signs that Japan’s ruling coalition may lose its parliamentary majority, which could give more power to opposition groups pushing for cuts to the consumption tax to ease the strain of inflation.

Inflation data out Friday showed core CPI in Japan eased slightly in June but still remained above the Bank of Japan’s 2% goal.

Aussie, Yuan Also Active

In other currencies, the Australian dollar gained 0.5% to 0.6516, rebounding after falling to its lowest point in over three weeks following weaker-than-expected employment data, which heightened bets on a Reserve Bank of Australia rate cut.

The Chinese yuan also saw minor movement, with USD/CNY dipping 0.1% to 7.1782.

This content is for informational purposes only and does not constitute financial, investment, or other professional advice. It should not be considered a recommendation to buy or sell any securities or financial instruments. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.