Delta Gold Technologies PLC (AQSE:DGQ) (USOTC:DGQTF), a company focused on developing intellectual property in quantum computing, has agreed to bring forward C$269,000 in research funding to the University of Toronto, advancing part of its Year 2 sponsorship commitment ahead of the planned July 2026 timetable. The payment forms part of a broader C$1 million second-year funding obligation and reflects encouraging progress achieved by the university’s research team.

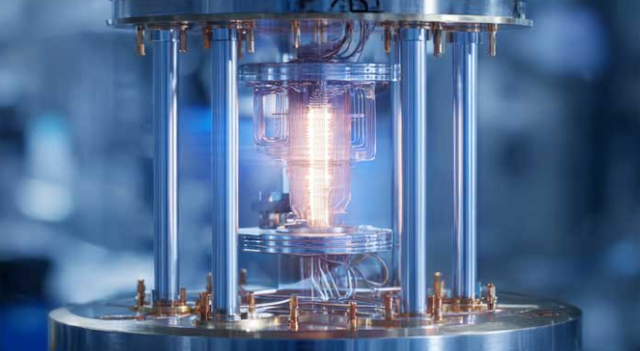

The early release of funds will support the integration of an additional component into the project’s cryogenic refrigeration system. This specialised system enables experiments to be conducted at ultra-low temperatures, creating stable environments required to test nano-scale material structures. Researchers are aiming to demonstrate foundational elements of a stable qubit using nano-scale gold combined with other materials. Achieving qubit stability remains one of the major technical challenges in quantum computing, underscoring the significance of the ongoing programme supported by Delta Gold.

Chief executive R. Michael Jones said: “We are pleased with the progress being made at the University of Toronto in our research using gold and other materials. Because of this, we have made the decision to make this advance which allows the research team to accelerate the experiments using the materials we have been designing and fabricating. I recently visited the lab at University of Toronto with our Principal Investigator Prof. Harry Ruda and it was amazing to see materials being worked on at the atomic level.”

Research partnership framework

Under the research sponsorship agreement, Delta Gold has committed to providing CAD $3 million in funding over three years to the University of Toronto. The arrangement grants the company exclusive rights to a 100% global licence for any intellectual property generated through the programme. The first-year payment of C$1 million has already been completed.

Leadership update

Delta Gold has also invited current non-executive director James Tosh to take on the role of executive director. In the expanded position, he is expected to work closely with CEO Michael Jones to advance operational execution and strategic development as the company moves toward commercialising its quantum computing technologies.

About Delta Gold Technologies

Delta Gold Technologies is developing intellectual property for applications within the quantum computing sector, centred on nano-scale gold and other advanced materials. The company collaborates with leading nanotechnology and quantum research groups worldwide to create patentable innovations intended for global licensing and commercial deployment within the rapidly evolving quantum computing industry.